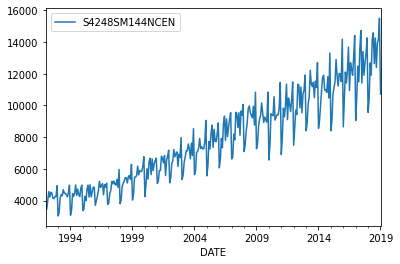

Time series - Alcohol Sales

Alcohol Sales

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import warnings

warnings.filterwarnings('ignore')

df = pd.read_csv('./Data/Alcohol_Sales.csv', index_col='DATE', parse_dates=True)

df.index.freq = 'MS'

df.info()

<class 'pandas.core.frame.DataFrame'>

DatetimeIndex: 325 entries, 1992-01-01 to 2019-01-01

Freq: MS

Data columns (total 1 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 S4248SM144NCEN 325 non-null int64

dtypes: int64(1)

memory usage: 5.1 KB

df.plot()

plt.show()

General Forecasting Model

from statsmodels.tsa.holtwinters import ExponentialSmoothing

from sklearn.metrics import mean_absolute_error, mean_squared_error

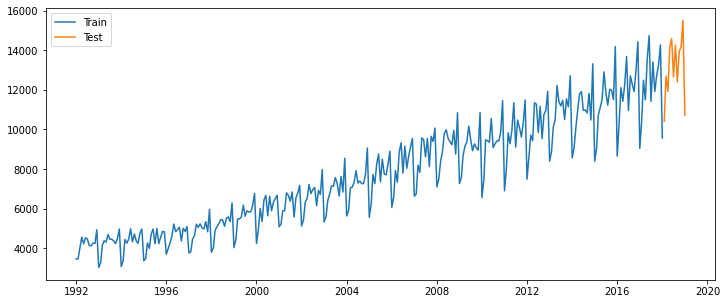

train_data = df.iloc[:-12]

test_data = df.iloc[-12:]

print(df.shape)

print(train_data.shape)

print(test_data.shape)

(325, 1)

(313, 1)

(12, 1)

fitted_model_mm = ExponentialSmoothing(train_data, trend='mul', seasonal='mul',seasonal_periods=12).fit()

fitted_model_aa = ExponentialSmoothing(train_data, trend='add', seasonal='add',seasonal_periods=12).fit()

c:\users\ilvna\.conda\envs\tf\lib\site-packages\statsmodels\tsa\holtwinters\model.py:922: ConvergenceWarning: Optimization failed to converge. Check mle_retvals.

ConvergenceWarning,

test_predictions_mm = fitted_model.forecast(12)

test_predictions_aa = fitted_model.forecast(12)

plt.figure(figsize=(12,5))

plt.plot(train_data, label='Train')

plt.plot(test_data, label='Test')

plt.legend()

plt.show()

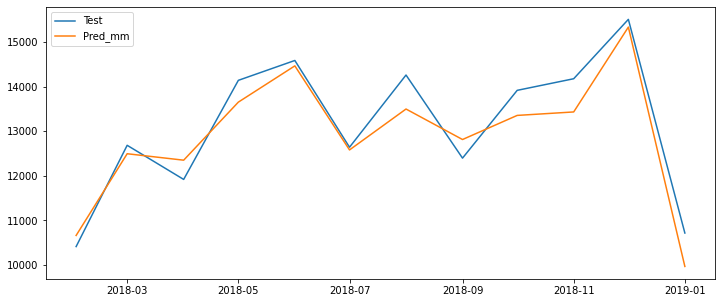

plt.figure(figsize=(12,5))

plt.plot(test_data, label='Test')

plt.plot(test_predictions_mm, label='Pred_mm')

plt.legend()

plt.show()

mae = mean_absolute_error(test_data, test_predictions)

mse = mean_squared_error(test_data ,test_predictions)

rmse = np.sqrt(mse)

print('mae :', mae)

print('mse :', mse)

print('rmse :', rmse)

mae : 411.9015865536535

mse : 229275.45568794024

rmse : 478.82716682320796

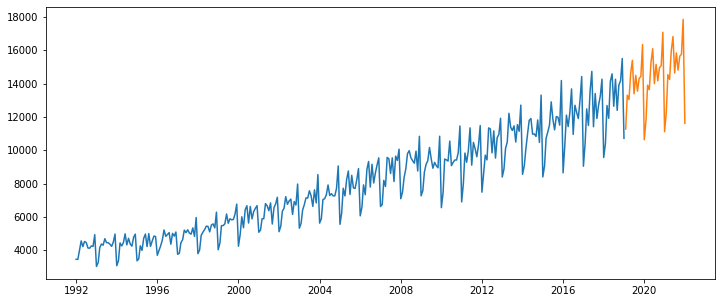

final_model = ExponentialSmoothing(df, trend='mul', seasonal='mul', seasonal_periods=12).fit()

c:\users\ilvna\.conda\envs\tf\lib\site-packages\statsmodels\tsa\holtwinters\model.py:922: ConvergenceWarning: Optimization failed to converge. Check mle_retvals.

ConvergenceWarning,

forecast_prediction = final_model.forecast(36)

plt.figure(figsize=(12,5))

plt.plot(df)

plt.plot(forecast_prediction)

plt.show()

ARIMA

from statsmodels.tsa.stattools import adfuller

from pmdarima import auto_arima

from statsmodels.tsa.arima_model import ARMA, ARIMA, ARMAResults, ARIMAResults

from statsmodels.tsa.statespace.sarimax import SARIMAX, SARIMAXResults

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

from statsmodels.tsa.statespace.tools import diff

from statsmodels.tsa.seasonal import seasonal_decompose

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

from statsmodels.tools.eval_measures import rmse

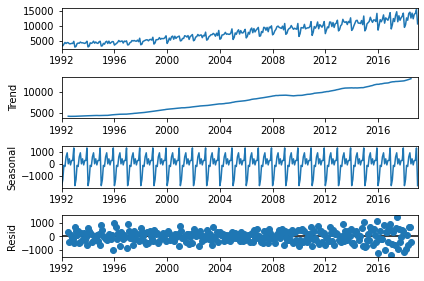

result = seasonal_decompose(df, model='add')

result.plot()

plt.show()

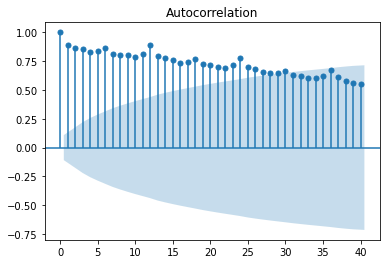

plot_acf(df, lags=40)

plt.show()

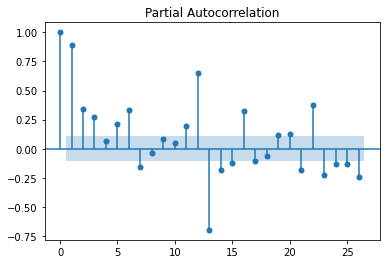

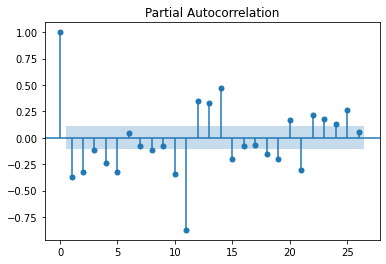

plot_pacf(df)

plt.show()

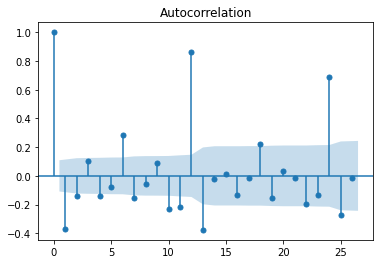

df_log = np.log(df)

df_log_diff = diff(df_log)

plot_acf(df_log_diff)

plot_pacf(df_log_diff)

plt.show()

print('p-value is : {}'.format(adfuller(df)[1]))

p-value is : 0.9987196267088919

isn’t stationary

df_diff = diff(df, k_diff=1)

print('p-value is : {}'.format(adfuller(df_diff)[1]))

p-value is : 0.0003408284921168574

is stationary

auto_arima

stepwise_fit = auto_arima(df, seasonal=True, trace=True, m=12)

Performing stepwise search to minimize aic

ARIMA(2,1,2)(1,1,1)[12] : AIC=4514.024, Time=1.35 sec

ARIMA(0,1,0)(0,1,0)[12] : AIC=4868.181, Time=0.01 sec

ARIMA(1,1,0)(1,1,0)[12] : AIC=4731.674, Time=0.08 sec

ARIMA(0,1,1)(0,1,1)[12] : AIC=4629.449, Time=0.66 sec

ARIMA(2,1,2)(0,1,1)[12] : AIC=4527.109, Time=0.79 sec

ARIMA(2,1,2)(1,1,0)[12] : AIC=4539.016, Time=0.39 sec

ARIMA(2,1,2)(2,1,1)[12] : AIC=4499.168, Time=4.80 sec

ARIMA(2,1,2)(2,1,0)[12] : AIC=4523.762, Time=1.18 sec

ARIMA(2,1,2)(2,1,2)[12] : AIC=inf, Time=7.26 sec

ARIMA(2,1,2)(1,1,2)[12] : AIC=4508.118, Time=4.54 sec

ARIMA(1,1,2)(2,1,1)[12] : AIC=4526.711, Time=5.72 sec

ARIMA(2,1,1)(2,1,1)[12] : AIC=4504.012, Time=3.65 sec

ARIMA(3,1,2)(2,1,1)[12] : AIC=4491.408, Time=5.70 sec

ARIMA(3,1,2)(1,1,1)[12] : AIC=4506.197, Time=2.39 sec

ARIMA(3,1,2)(2,1,0)[12] : AIC=4514.299, Time=4.16 sec

ARIMA(3,1,2)(2,1,2)[12] : AIC=4444.011, Time=7.65 sec

ARIMA(3,1,2)(1,1,2)[12] : AIC=4499.385, Time=6.75 sec

ARIMA(3,1,1)(2,1,2)[12] : AIC=inf, Time=6.98 sec

ARIMA(4,1,2)(2,1,2)[12] : AIC=4460.069, Time=9.64 sec

ARIMA(3,1,3)(2,1,2)[12] : AIC=4448.232, Time=9.26 sec

ARIMA(2,1,1)(2,1,2)[12] : AIC=inf, Time=6.27 sec

ARIMA(2,1,3)(2,1,2)[12] : AIC=4449.248, Time=8.97 sec

ARIMA(4,1,1)(2,1,2)[12] : AIC=inf, Time=8.59 sec

ARIMA(4,1,3)(2,1,2)[12] : AIC=4460.041, Time=10.26 sec

ARIMA(3,1,2)(2,1,2)[12] intercept : AIC=4462.884, Time=8.87 sec

Best model: ARIMA(3,1,2)(2,1,2)[12]

Total fit time: 125.962 seconds

stepwise_fit.summary()

| Dep. Variable: | y | No. Observations: | 325 |

|---|---|---|---|

| Model: | SARIMAX(3, 1, 2)x(2, 1, 2, 12) | Log Likelihood | -2212.006 |

| Date: | Fri, 09 Apr 2021 | AIC | 4444.011 |

| Time: | 11:46:26 | BIC | 4481.441 |

| Sample: | 0 | HQIC | 4458.971 |

| - 325 | |||

| Covariance Type: | opg |

| coef | std err | z | P>|z| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| ar.L1 | -0.0899 | 0.215 | -0.418 | 0.676 | -0.512 | 0.332 |

| ar.L2 | 0.0985 | 0.087 | 1.128 | 0.259 | -0.073 | 0.270 |

| ar.L3 | 0.3208 | 0.069 | 4.639 | 0.000 | 0.185 | 0.456 |

| ma.L1 | -0.7431 | 0.223 | -3.335 | 0.001 | -1.180 | -0.306 |

| ma.L2 | -0.1539 | 0.182 | -0.845 | 0.398 | -0.511 | 0.203 |

| ar.S.L12 | 0.8702 | 0.068 | 12.850 | 0.000 | 0.737 | 1.003 |

| ar.S.L24 | -0.8249 | 0.059 | -13.973 | 0.000 | -0.941 | -0.709 |

| ma.S.L12 | -1.1483 | 0.100 | -11.534 | 0.000 | -1.343 | -0.953 |

| ma.S.L24 | 0.6663 | 0.096 | 6.959 | 0.000 | 0.479 | 0.854 |

| sigma2 | 8.337e+04 | 6834.224 | 12.199 | 0.000 | 7e+04 | 9.68e+04 |

| Ljung-Box (L1) (Q): | 0.18 | Jarque-Bera (JB): | 10.24 |

|---|---|---|---|

| Prob(Q): | 0.67 | Prob(JB): | 0.01 |

| Heteroskedasticity (H): | 4.23 | Skew: | -0.11 |

| Prob(H) (two-sided): | 0.00 | Kurtosis: | 3.86 |

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

model = SARIMAX(train_data, order=(3,1,2), seasonal_order=(2,1,2,12))

results = model.fit()

c:\users\ilvna\.conda\envs\tf\lib\site-packages\statsmodels\base\model.py:568: ConvergenceWarning: Maximum Likelihood optimization failed to converge. Check mle_retvals

ConvergenceWarning)

results.summary()

| Dep. Variable: | S4248SM144NCEN | No. Observations: | 313 |

|---|---|---|---|

| Model: | SARIMAX(3, 1, 2)x(2, 1, 2, 12) | Log Likelihood | -2130.091 |

| Date: | Fri, 09 Apr 2021 | AIC | 4280.183 |

| Time: | 11:47:17 | BIC | 4317.221 |

| Sample: | 01-01-1992 | HQIC | 4295.005 |

| - 01-01-2018 | |||

| Covariance Type: | opg |

| coef | std err | z | P>|z| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| ar.L1 | -0.2578 | 0.223 | -1.158 | 0.247 | -0.694 | 0.178 |

| ar.L2 | 0.0882 | 0.104 | 0.845 | 0.398 | -0.116 | 0.293 |

| ar.L3 | 0.3605 | 0.085 | 4.235 | 0.000 | 0.194 | 0.527 |

| ma.L1 | -0.6401 | 0.225 | -2.844 | 0.004 | -1.081 | -0.199 |

| ma.L2 | -0.2576 | 0.188 | -1.373 | 0.170 | -0.625 | 0.110 |

| ar.S.L12 | 0.8397 | 0.124 | 6.754 | 0.000 | 0.596 | 1.083 |

| ar.S.L24 | -0.7472 | 0.087 | -8.554 | 0.000 | -0.918 | -0.576 |

| ma.S.L12 | -1.1464 | 0.158 | -7.235 | 0.000 | -1.457 | -0.836 |

| ma.S.L24 | 0.6295 | 0.149 | 4.230 | 0.000 | 0.338 | 0.921 |

| sigma2 | 1.02e+05 | 1.01e+04 | 10.119 | 0.000 | 8.22e+04 | 1.22e+05 |

| Ljung-Box (L1) (Q): | 0.17 | Jarque-Bera (JB): | 9.97 |

|---|---|---|---|

| Prob(Q): | 0.68 | Prob(JB): | 0.01 |

| Heteroskedasticity (H): | 4.70 | Skew: | -0.12 |

| Prob(H) (two-sided): | 0.00 | Kurtosis: | 3.86 |

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

start = len(train_data)

end = len(train_data) + len(test_data) - 1

pred = results.predict(start, end, typ='level')

plt.plot(test_data)

plt.plot(pred)

plt.show()

error = rmse(test_data, pred)

error

array([2854.34960749, 1718.78826431, 1867.1512623 , 1812.19483997,

2065.05758019, 1687.09691322, 1590.03025873, 1711.93822433,

1559.00525313, 1517.72740288, 2247.46882941, 3260.6541987 ])

model = SARIMAX(df, order=(3,1,2), seasonal_order=(2,1,2,12))

results = model.fit()

c:\users\ilvna\.conda\envs\tf\lib\site-packages\statsmodels\base\model.py:568: ConvergenceWarning: Maximum Likelihood optimization failed to converge. Check mle_retvals

ConvergenceWarning)

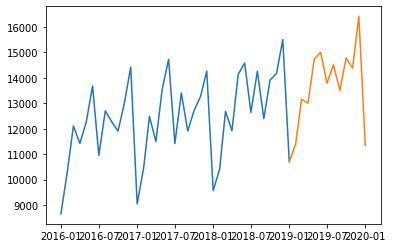

forecast = results.predict(len(df)-1, len(df)+11, typ='levels')

plt.plot(df['2016-01-01':])

plt.plot(forecast)

plt.show()

LSTM

from tensorflow.keras.preprocessing.sequence import TimeseriesGenerator

from sklearn.preprocessing import MinMaxScaler

from tensorflow.keras.models import Model

from tensorflow.keras.layers import Dense, LSTM, Input

nobs = 12

train = df.iloc[:-nobs]

test = df.iloc[-nobs:]

scaler = MinMaxScaler()

scaler.fit(train)

MinMaxScaler()

scaled_train = scaler.transform(train)

scaled_test = scaler.transform(test)

n_input = 12

n_features = 1

gen = TimeseriesGenerator(scaled_train, scaled_train, length=n_input, batch_size=1)

print(len(scaled_train))

print(len(scaled_test))

print(len(gen))

313

12

301

X, y = gen[0]

X, y

(array([[[0.03658432],

[0.03649885],

[0.08299855],

[0.13103684],

[0.1017181 ],

[0.12804513],

[0.12266006],

[0.09453799],

[0.09359774],

[0.10496624],

[0.10334217],

[0.16283443]]]),

array([[0.]]))

inputs = Input(shape=(n_input, n_features))

x = LSTM(150, activation='relu')(inputs)

x = Dense(1)(x)

WARNING:tensorflow:Layer lstm will not use cuDNN kernel since it doesn't meet the cuDNN kernel criteria. It will use generic GPU kernel as fallback when running on GPU

model = Model(inputs, x)

model.summary()

Model: "functional_1"

_________________________________________________________________

Layer (type) Output Shape Param #

=================================================================

input_1 (InputLayer) [(None, 12, 1)] 0

_________________________________________________________________

lstm (LSTM) (None, 150) 91200

_________________________________________________________________

dense (Dense) (None, 1) 151

=================================================================

Total params: 91,351

Trainable params: 91,351

Non-trainable params: 0

_________________________________________________________________

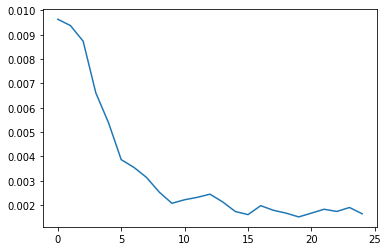

model.compile(optimizer='adam', loss='mse')

history = model.fit_generator(gen, epochs = 25)

Epoch 1/25

301/301 [==============================] - 5s 16ms/step - loss: 0.0096

Epoch 2/25

301/301 [==============================] - 5s 16ms/step - loss: 0.0094

Epoch 3/25

301/301 [==============================] - 5s 16ms/step - loss: 0.0087

Epoch 4/25

301/301 [==============================] - 5s 16ms/step - loss: 0.0066

Epoch 5/25

301/301 [==============================] - 5s 16ms/step - loss: 0.0054

Epoch 6/25

301/301 [==============================] - 5s 16ms/step - loss: 0.0039

Epoch 7/25

301/301 [==============================] - 5s 16ms/step - loss: 0.0035

Epoch 8/25

301/301 [==============================] - 5s 16ms/step - loss: 0.0031: 0s

Epoch 9/25

301/301 [==============================] - 5s 16ms/step - loss: 0.0025

Epoch 10/25

301/301 [==============================] - 5s 16ms/step - loss: 0.0021

Epoch 11/25

301/301 [==============================] - 5s 16ms/step - loss: 0.0022

Epoch 12/25

301/301 [==============================] - 5s 17ms/step - loss: 0.0023

Epoch 13/25

301/301 [==============================] - 5s 17ms/step - loss: 0.0024

Epoch 14/25

301/301 [==============================] - 5s 17ms/step - loss: 0.0021

Epoch 15/25

301/301 [==============================] - 5s 17ms/step - loss: 0.0017

Epoch 16/25

301/301 [==============================] - 5s 17ms/step - loss: 0.0016

Epoch 17/25

301/301 [==============================] - 5s 17ms/step - loss: 0.0020

Epoch 18/25

301/301 [==============================] - 5s 17ms/step - loss: 0.0018

Epoch 19/25

301/301 [==============================] - 5s 17ms/step - loss: 0.0017

Epoch 20/25

301/301 [==============================] - 5s 17ms/step - loss: 0.0015

Epoch 21/25

301/301 [==============================] - 5s 17ms/step - loss: 0.0017

Epoch 22/25

301/301 [==============================] - 5s 17ms/step - loss: 0.0018

Epoch 23/25

301/301 [==============================] - 5s 17ms/step - loss: 0.0017

Epoch 24/25

301/301 [==============================] - 5s 17ms/step - loss: 0.0019

Epoch 25/25

301/301 [==============================] - 5s 17ms/step - loss: 0.0016

plt.plot(range(len(history.history['loss'])), model.history.history['loss'])

[<matplotlib.lines.Line2D at 0x24121def0c8>]

first_eval_batch = scaled_train[-12:]

first_eval_batch = first_eval_batch.reshape((1, n_input, n_features))

model.predict(first_eval_batch)

array([[0.78138685]], dtype=float32)

Forecast

test_predictions = []

first_eval_batch = scaled_train[-n_input:]

current_batch = first_eval_batch.reshape((1, n_input, n_features))

for i in range(len(test)):

current_pred = model.predict(current_batch)[0]

test_predictions.append(current_pred)

current_batch = np.append(current_batch[:,1:,:], [[current_pred]], axis=1)

test_predictions

[array([0.78138685], dtype=float32),

array([0.9095711], dtype=float32),

array([0.85770994], dtype=float32),

array([1.0188285], dtype=float32),

array([1.0919129], dtype=float32),

array([0.84825593], dtype=float32),

array([1.001781], dtype=float32),

array([0.87678725], dtype=float32),

array([0.9534033], dtype=float32),

array([0.9890802], dtype=float32),

array([1.060493], dtype=float32),

array([0.696439], dtype=float32)]

true_predictions = scaler.inverse_transform(test_predictions)

true_predictions

array([[12172.44478464],

[13672.07242996],

[13065.34863776],

[14950.27475297],

[15805.28861511],

[12954.74615234],

[14750.83576441],

[13288.53398246],

[14184.86513752],

[14602.24915051],

[15437.7075181 ],

[11178.64018607]])

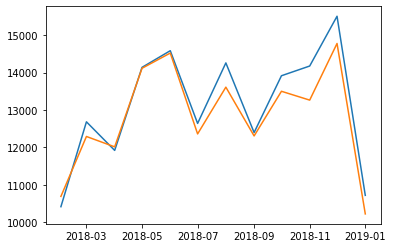

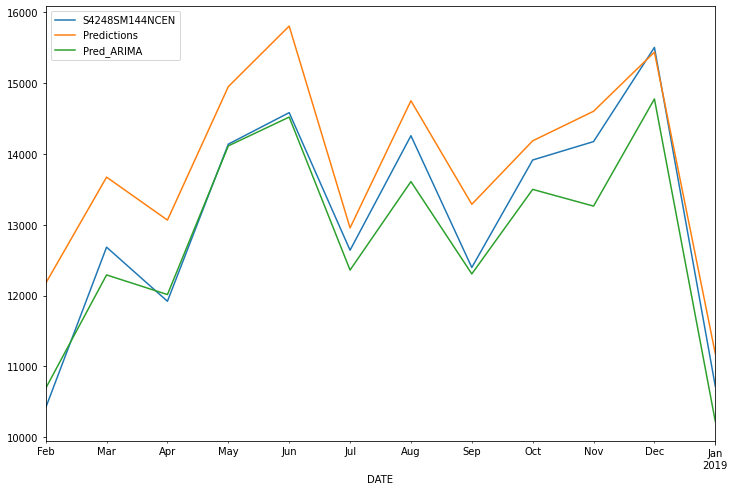

test['Predictions'] = true_predictions

test

| S4248SM144NCEN | Predictions | |

|---|---|---|

| DATE | ||

| 2018-02-01 | 10415 | 12172.444785 |

| 2018-03-01 | 12683 | 13672.072430 |

| 2018-04-01 | 11919 | 13065.348638 |

| 2018-05-01 | 14138 | 14950.274753 |

| 2018-06-01 | 14583 | 15805.288615 |

| 2018-07-01 | 12640 | 12954.746152 |

| 2018-08-01 | 14257 | 14750.835764 |

| 2018-09-01 | 12396 | 13288.533982 |

| 2018-10-01 | 13914 | 14184.865138 |

| 2018-11-01 | 14174 | 14602.249151 |

| 2018-12-01 | 15504 | 15437.707518 |

| 2019-01-01 | 10718 | 11178.640186 |

test.plot(figsize=(12,8))

<AxesSubplot:xlabel='DATE'>

test['Pred_ARIMA'] = pred

print(rmse(test['S4248SM144NCEN'], test['Predictions']))

print(rmse(test['S4248SM144NCEN'], test['Pred_ARIMA']))

873.1015843567056

458.91865971479376