Time Series Analysis - Time Series Analysis with Statsmodels

Time Series Analysis with Statsmodels

import numpy as np

import pandas as pd

%matplotlib inline

import matplotlib.pyplot as plt

df = pd.read_csv('Data/macrodata.csv', index_col = 0, parse_dates = True)

df.head()

| year | quarter | realgdp | realcons | realinv | realgovt | realdpi | cpi | m1 | tbilrate | unemp | pop | infl | realint | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1959-03-31 | 1959 | 1 | 2710.349 | 1707.4 | 286.898 | 470.045 | 1886.9 | 28.98 | 139.7 | 2.82 | 5.8 | 177.146 | 0.00 | 0.00 |

| 1959-06-30 | 1959 | 2 | 2778.801 | 1733.7 | 310.859 | 481.301 | 1919.7 | 29.15 | 141.7 | 3.08 | 5.1 | 177.830 | 2.34 | 0.74 |

| 1959-09-30 | 1959 | 3 | 2775.488 | 1751.8 | 289.226 | 491.260 | 1916.4 | 29.35 | 140.5 | 3.82 | 5.3 | 178.657 | 2.74 | 1.09 |

| 1959-12-31 | 1959 | 4 | 2785.204 | 1753.7 | 299.356 | 484.052 | 1931.3 | 29.37 | 140.0 | 4.33 | 5.6 | 179.386 | 0.27 | 4.06 |

| 1960-03-31 | 1960 | 1 | 2847.699 | 1770.5 | 331.722 | 462.199 | 1955.5 | 29.54 | 139.6 | 3.50 | 5.2 | 180.007 | 2.31 | 1.19 |

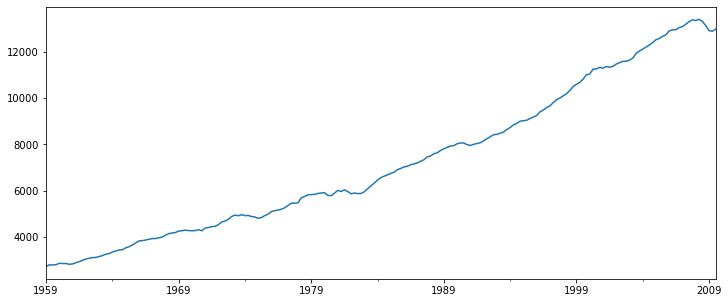

df['realgdp'].plot(figsize =(12,5))

<AxesSubplot:>

from statsmodels.tsa.filters.hp_filter import hpfilter

gdp_cycle, gdp_trend = hpfilter(df['realgdp'])

type(gdp_trend)

pandas.core.series.Series

df['trend'] = gdp_trend

df.head()

| year | quarter | realgdp | realcons | realinv | realgovt | realdpi | cpi | m1 | tbilrate | unemp | pop | infl | realint | trend | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1959-03-31 | 1959 | 1 | 2710.349 | 1707.4 | 286.898 | 470.045 | 1886.9 | 28.98 | 139.7 | 2.82 | 5.8 | 177.146 | 0.00 | 0.00 | 2670.837085 |

| 1959-06-30 | 1959 | 2 | 2778.801 | 1733.7 | 310.859 | 481.301 | 1919.7 | 29.15 | 141.7 | 3.08 | 5.1 | 177.830 | 2.34 | 0.74 | 2698.712468 |

| 1959-09-30 | 1959 | 3 | 2775.488 | 1751.8 | 289.226 | 491.260 | 1916.4 | 29.35 | 140.5 | 3.82 | 5.3 | 178.657 | 2.74 | 1.09 | 2726.612545 |

| 1959-12-31 | 1959 | 4 | 2785.204 | 1753.7 | 299.356 | 484.052 | 1931.3 | 29.37 | 140.0 | 4.33 | 5.6 | 179.386 | 0.27 | 4.06 | 2754.612067 |

| 1960-03-31 | 1960 | 1 | 2847.699 | 1770.5 | 331.722 | 462.199 | 1955.5 | 29.54 | 139.6 | 3.50 | 5.2 | 180.007 | 2.31 | 1.19 | 2782.816333 |

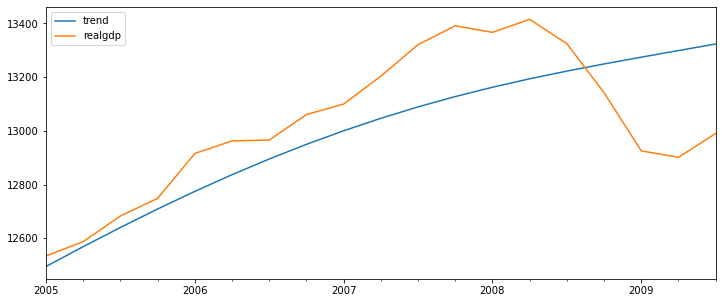

df[['trend','realgdp']]['2005-01-01':].plot(figsize = (12, 5))

<AxesSubplot:>

ETS Models

airline = pd.read_csv('Data/airline_passengers.csv', index_col = 'Month', parse_dates=True)

airline = airline.dropna()

airline.head()

| Thousands of Passengers | |

|---|---|

| Month | |

| 1949-01-01 | 112 |

| 1949-02-01 | 118 |

| 1949-03-01 | 132 |

| 1949-04-01 | 129 |

| 1949-05-01 | 121 |

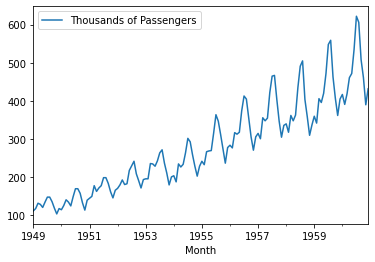

airline.plot()

<AxesSubplot:xlabel='Month'>

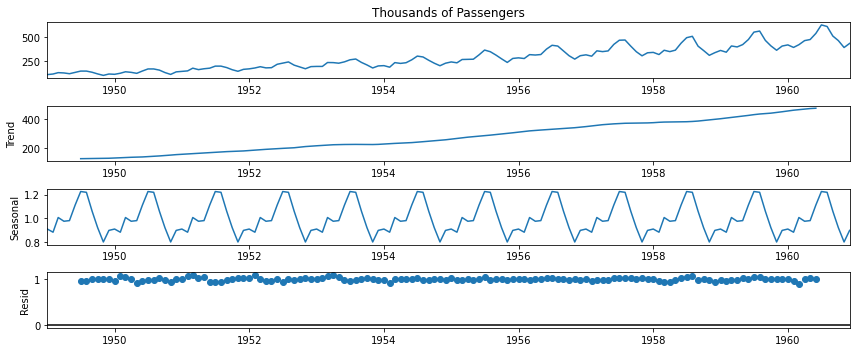

from statsmodels.tsa.seasonal import seasonal_decompose

result = seasonal_decompose(airline['Thousands of Passengers'], model='multiplicative')

from pylab import rcParams

rcParams['figure.figsize'] = 12,5

result.plot();

EWMA Models

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

%matplotlib inline

airline = pd.read_csv('Data/airline_passengers.csv', index_col="Month")

airline.dropna(inplace=True)

airline.index = pd.to_datetime(airline.index)

airline.index

DatetimeIndex(['1949-01-01', '1949-02-01', '1949-03-01', '1949-04-01',

'1949-05-01', '1949-06-01', '1949-07-01', '1949-08-01',

'1949-09-01', '1949-10-01',

...

'1960-03-01', '1960-04-01', '1960-05-01', '1960-06-01',

'1960-07-01', '1960-08-01', '1960-09-01', '1960-10-01',

'1960-11-01', '1960-12-01'],

dtype='datetime64[ns]', name='Month', length=144, freq=None)

airline.head()

| Thousands of Passengers | |

|---|---|

| Month | |

| 1949-01-01 | 112 |

| 1949-02-01 | 118 |

| 1949-03-01 | 132 |

| 1949-04-01 | 129 |

| 1949-05-01 | 121 |

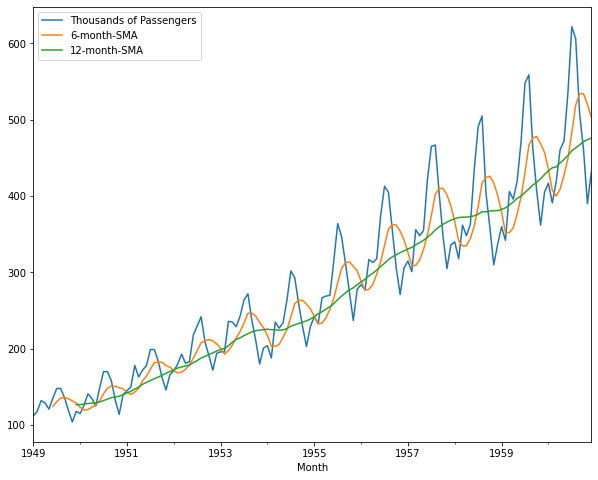

airline['6-month-SMA'] = airline['Thousands of Passengers'].rolling(window=6).mean()

airline['12-month-SMA'] = airline['Thousands of Passengers'].rolling(window=12).mean()

airline.plot(figsize = (10, 8));

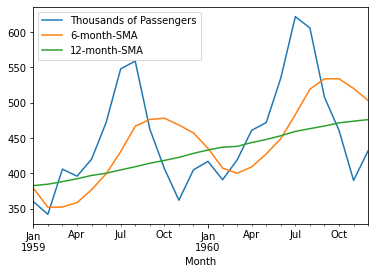

airline['1959':].plot();

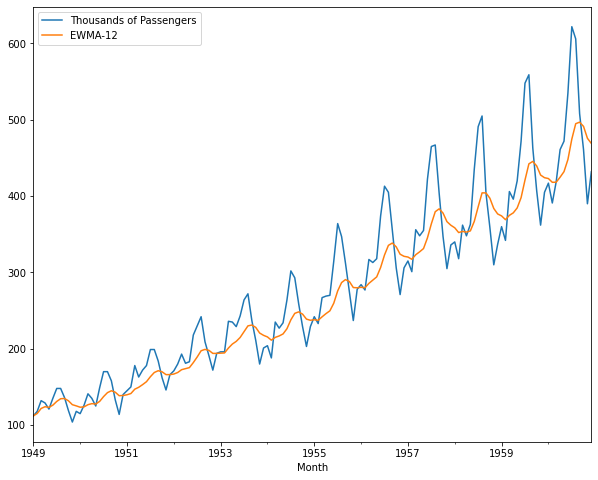

airline['EWMA-12'] = airline['Thousands of Passengers'].ewm(span = 12).mean()

airline[['Thousands of Passengers','EWMA-12']].plot(figsize = (10, 8))

<AxesSubplot:xlabel='Month'>

Holt - Winters Methods

import numpy as np

import pandas as pd

%matplotlib inline

df = pd.read_csv('Data/airline_passengers.csv', index_col = 'Month', parse_dates=True)

df = df.dropna()

df.index

DatetimeIndex(['1949-01-01', '1949-02-01', '1949-03-01', '1949-04-01',

'1949-05-01', '1949-06-01', '1949-07-01', '1949-08-01',

'1949-09-01', '1949-10-01',

...

'1960-03-01', '1960-04-01', '1960-05-01', '1960-06-01',

'1960-07-01', '1960-08-01', '1960-09-01', '1960-10-01',

'1960-11-01', '1960-12-01'],

dtype='datetime64[ns]', name='Month', length=144, freq=None)

df.index.freq = 'MS'

df.index

DatetimeIndex(['1949-01-01', '1949-02-01', '1949-03-01', '1949-04-01',

'1949-05-01', '1949-06-01', '1949-07-01', '1949-08-01',

'1949-09-01', '1949-10-01',

...

'1960-03-01', '1960-04-01', '1960-05-01', '1960-06-01',

'1960-07-01', '1960-08-01', '1960-09-01', '1960-10-01',

'1960-11-01', '1960-12-01'],

dtype='datetime64[ns]', name='Month', length=144, freq='MS')

df.head()

| Thousands of Passengers | |

|---|---|

| Month | |

| 1949-01-01 | 112 |

| 1949-02-01 | 118 |

| 1949-03-01 | 132 |

| 1949-04-01 | 129 |

| 1949-05-01 | 121 |

from statsmodels.tsa.holtwinters import SimpleExpSmoothing

span = 12

alpha = 2/(span+1)

df['EWMA12'] = df['Thousands of Passengers'].ewm(alpha = alpha, adjust = False).mean()

df.head()

| Thousands of Passengers | EWMA12 | |

|---|---|---|

| Month | ||

| 1949-01-01 | 112 | 112.000000 |

| 1949-02-01 | 118 | 112.923077 |

| 1949-03-01 | 132 | 115.857988 |

| 1949-04-01 | 129 | 117.879836 |

| 1949-05-01 | 121 | 118.359861 |

model = SimpleExpSmoothing(df['Thousands of Passengers'])

C:\Users\ilvna\.conda\envs\tf-2.3\lib\site-packages\statsmodels\tsa\holtwinters\model.py:429: FutureWarning: After 0.13 initialization must be handled at model creation

FutureWarning,

fitted_model = model.fit(smoothing_level=alpha, optimized=False)

df['SES12'] = fitted_model.fittedvalues.shift(-1)

df.head()

| Thousands of Passengers | EWMA12 | SES12 | |

|---|---|---|---|

| Month | |||

| 1949-01-01 | 112 | 112.000000 | 112.000000 |

| 1949-02-01 | 118 | 112.923077 | 112.923077 |

| 1949-03-01 | 132 | 115.857988 | 115.857988 |

| 1949-04-01 | 129 | 117.879836 | 117.879836 |

| 1949-05-01 | 121 | 118.359861 | 118.359861 |

# df['SES12'] = SimpleExpSmoothing(df['Thousands of Passengers']).fit(smoothing_level=alpha, optimized=False).fittedvalues.shift(-1)

from statsmodels.tsa.holtwinters import ExponentialSmoothing

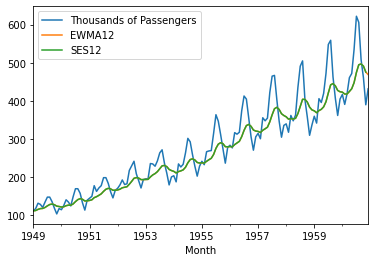

df.plot()

<AxesSubplot:xlabel='Month'>

df['DES_add_12'] = ExponentialSmoothing(df['Thousands of Passengers'],trend='add').fit().fittedvalues.shift(-1)

C:\Users\ilvna\.conda\envs\tf-2.3\lib\site-packages\statsmodels\tsa\holtwinters\model.py:429: FutureWarning: After 0.13 initialization must be handled at model creation

FutureWarning,

df['DES_mul_12'] = ExponentialSmoothing(df['Thousands of Passengers'],trend='mul').fit().fittedvalues.shift(-1)

C:\Users\ilvna\.conda\envs\tf-2.3\lib\site-packages\statsmodels\tsa\holtwinters\model.py:429: FutureWarning: After 0.13 initialization must be handled at model creation

FutureWarning,

df.head()

| Thousands of Passengers | EWMA12 | SES12 | DES_add_12 | DES_mul_12 | |

|---|---|---|---|---|---|

| Month | |||||

| 1949-01-01 | 112 | 112.000000 | 112.000000 | 114.221156 | 112.688538 |

| 1949-02-01 | 118 | 112.923077 | 112.923077 | 120.175837 | 118.725424 |

| 1949-03-01 | 132 | 115.857988 | 115.857988 | 134.115056 | 132.811491 |

| 1949-04-01 | 129 | 117.879836 | 117.879836 | 131.244976 | 129.793048 |

| 1949-05-01 | 121 | 118.359861 | 118.359861 | 123.283465 | 121.743867 |

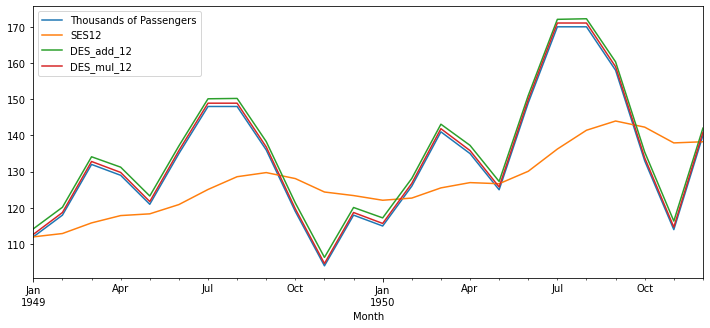

df[['Thousands of Passengers', 'SES12', 'DES_add_12','DES_mul_12']].iloc[:24].plot(figsize=(12,5))

<AxesSubplot:xlabel='Month'>

df['TES_mul_12']=ExponentialSmoothing(df['Thousands of Passengers'],trend='mul',seasonal='mul',seasonal_periods=12).fit().fittedvalues

C:\Users\ilvna\.conda\envs\tf-2.3\lib\site-packages\statsmodels\tsa\holtwinters\model.py:429: FutureWarning: After 0.13 initialization must be handled at model creation

FutureWarning,

C:\Users\ilvna\.conda\envs\tf-2.3\lib\site-packages\statsmodels\tsa\holtwinters\model.py:80: RuntimeWarning: overflow encountered in matmul

return err.T @ err

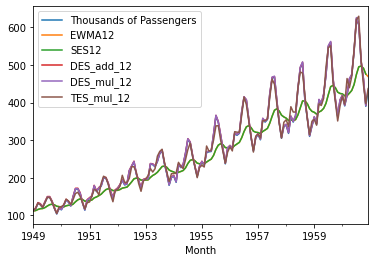

df.plot()

<AxesSubplot:xlabel='Month'>

df.columns

Index(['Thousands of Passengers', 'EWMA12', 'SES12', 'DES_add_12',

'DES_mul_12', 'TES_mul_12'],

dtype='object')

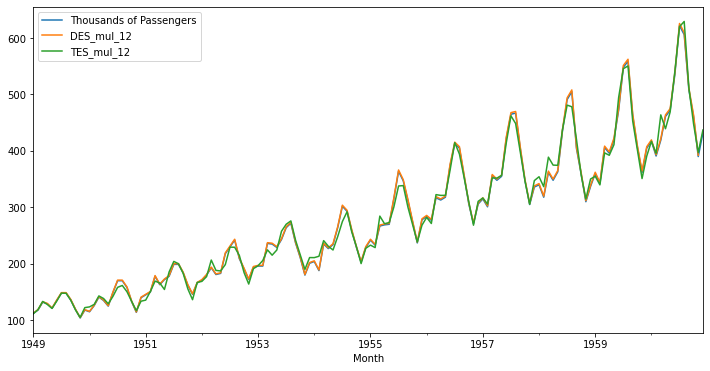

df[['Thousands of Passengers', 'DES_mul_12', 'TES_mul_12']].plot(figsize=(12,6))

<AxesSubplot:xlabel='Month'>

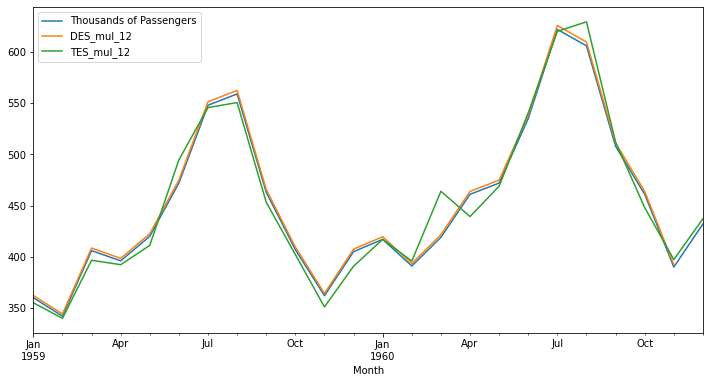

df[['Thousands of Passengers', 'DES_mul_12', 'TES_mul_12']].iloc[-24:].plot(figsize=(12,6))

<AxesSubplot:xlabel='Month'>