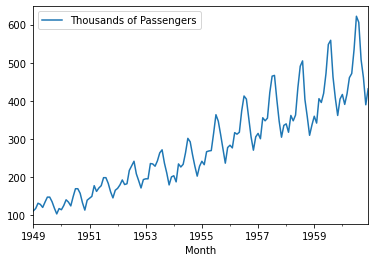

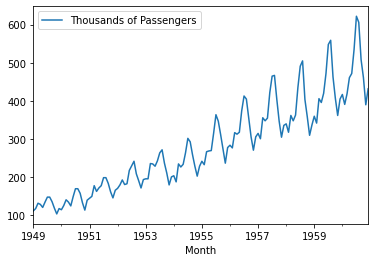

<class 'pandas.core.frame.DataFrame'>

DatetimeIndex: 144 entries, 1949-01-01 to 1960-12-01

Freq: MS

Data columns (total 1 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Thousands of Passengers 144 non-null int64

dtypes: int64(1)

memory usage: 2.2 KB

C:\Users\ilvna\.conda\envs\tf-2.3\lib\site-packages\statsmodels\tsa\holtwinters\model.py:429: FutureWarning: After 0.13 initialization must be handled at model creation

FutureWarning,

C:\Users\ilvna\.conda\envs\tf-2.3\lib\site-packages\statsmodels\tsa\holtwinters\model.py:80: RuntimeWarning: overflow encountered in matmul

return err.T @ err

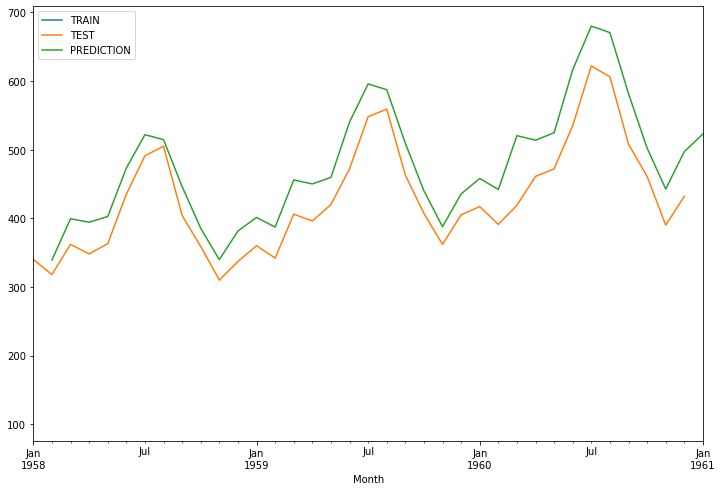

1958-02-01 339.142839

1958-03-01 399.281567

1958-04-01 394.233518

1958-05-01 402.545212

1958-06-01 473.128729

1958-07-01 521.795258

1958-08-01 514.513564

1958-09-01 446.216722

1958-10-01 385.430842

1958-11-01 339.645012

1958-12-01 381.455551

1959-01-01 401.210071

1959-02-01 387.159060

1959-03-01 455.812296

1959-04-01 450.049538

1959-05-01 459.538011

1959-06-01 540.114821

1959-07-01 595.671611

1959-08-01 587.358966

1959-09-01 509.392582

1959-10-01 440.000570

1959-11-01 387.732331

1959-12-01 435.462452

1960-01-01 458.013840

1960-02-01 441.973470

1960-03-01 520.346708

1960-04-01 513.768052

1960-05-01 524.599914

1960-06-01 616.584878

1960-07-01 680.007460

1960-08-01 670.517902

1960-09-01 581.512951

1960-10-01 502.296340

1960-11-01 442.627906

1960-12-01 497.115710

1961-01-01 522.859949

Freq: MS, dtype: float64

<AxesSubplot:xlabel='Month'>

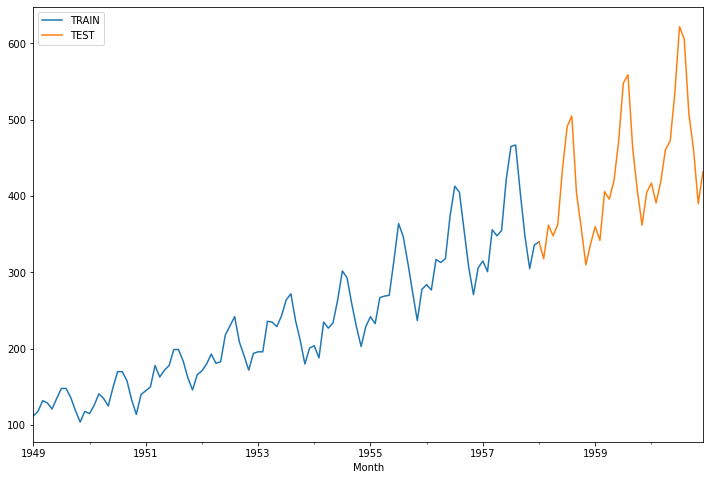

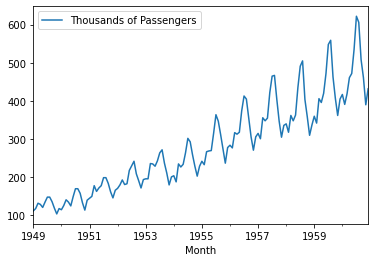

train_data['Thousands of Passengers'].plot(legend=True, label='TRAIN',figsize=(12,8))

test_data['Thousands of Passengers'].plot(legend=True, label='TEST')

test_predictions.plot(legend=True, label='PREDICTION',xlim=['1958-01-01','1961-01-01'])

<AxesSubplot:xlabel='Month'>

C:\Users\ilvna\.conda\envs\tf-2.3\lib\site-packages\statsmodels\tsa\holtwinters\model.py:429: FutureWarning: After 0.13 initialization must be handled at model creation

FutureWarning,

C:\Users\ilvna\.conda\envs\tf-2.3\lib\site-packages\statsmodels\tsa\holtwinters\model.py:80: RuntimeWarning: overflow encountered in matmul

return err.T @ err

<AxesSubplot:xlabel='Month'>

array([ 1. , -0.5 , -0.2 , 0.275, -0.075])

array([ 1. , -0.625 , -1.18803419, 2.03764205, 0.8949589 ])

array([ 1. , -0.49677419, -0.43181818, 0.53082621, 0.25434783])

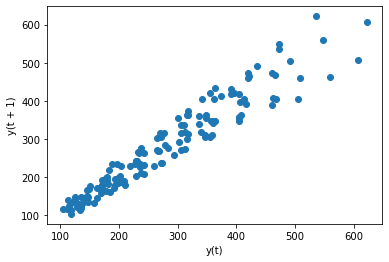

<AxesSubplot:xlabel='y(t)', ylabel='y(t + 1)'>

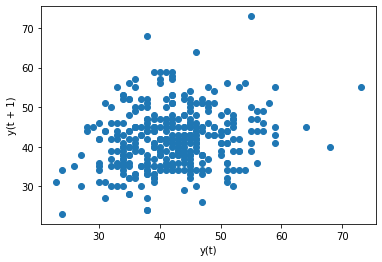

<AxesSubplot:xlabel='y(t)', ylabel='y(t + 1)'>

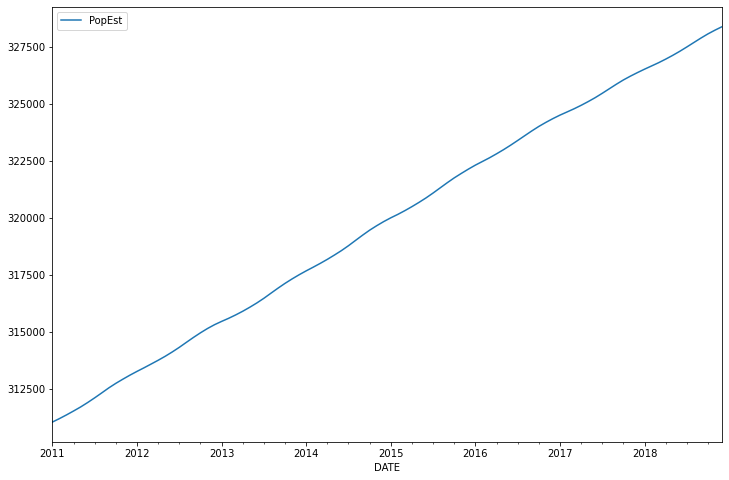

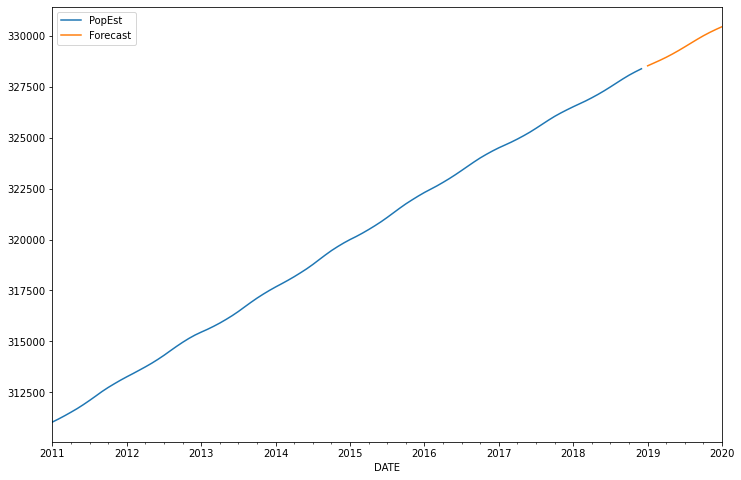

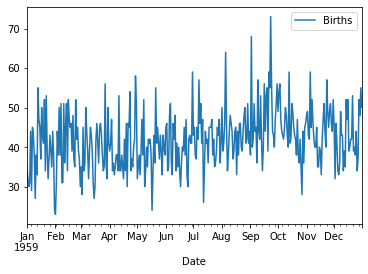

<AxesSubplot:xlabel='DATE'>

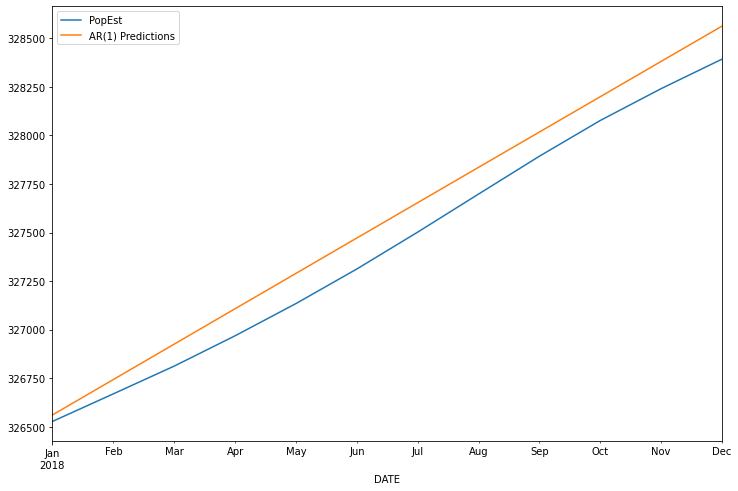

const 284.913797

L1.PopEst 0.999686

dtype: float64

2018-01-01 326560.403377

2018-02-01 326742.749463

2018-03-01 326925.038278

2018-04-01 327107.269838

2018-05-01 327289.444162

2018-06-01 327471.561268

2018-07-01 327653.621173

2018-08-01 327835.623896

2018-09-01 328017.569455

2018-10-01 328199.457868

2018-11-01 328381.289152

2018-12-01 328563.063326

Freq: MS, dtype: float64

2018-01-01 326560.403377

2018-02-01 326742.749463

2018-03-01 326925.038278

2018-04-01 327107.269838

2018-05-01 327289.444162

2018-06-01 327471.561268

2018-07-01 327653.621173

2018-08-01 327835.623896

2018-09-01 328017.569455

2018-10-01 328199.457868

2018-11-01 328381.289152

2018-12-01 328563.063326

Freq: MS, Name: AR(1) Predictions, dtype: float64

<AxesSubplot:xlabel='DATE'>

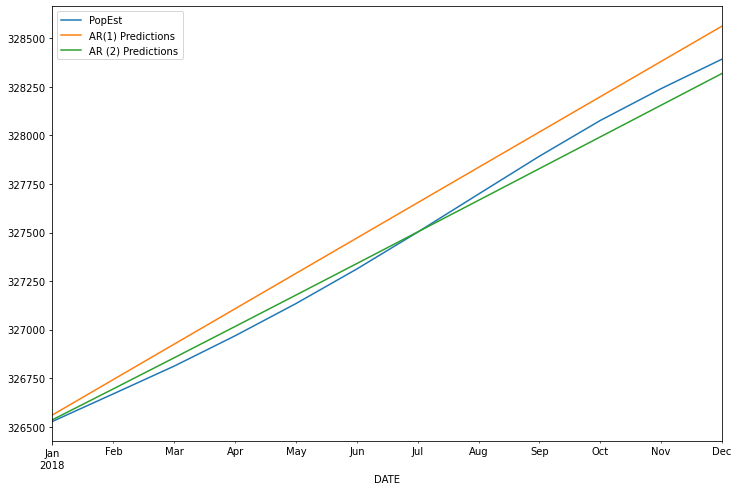

const 137.368305

L1.PopEst 1.853490

L2.PopEst -0.853836

dtype: float64

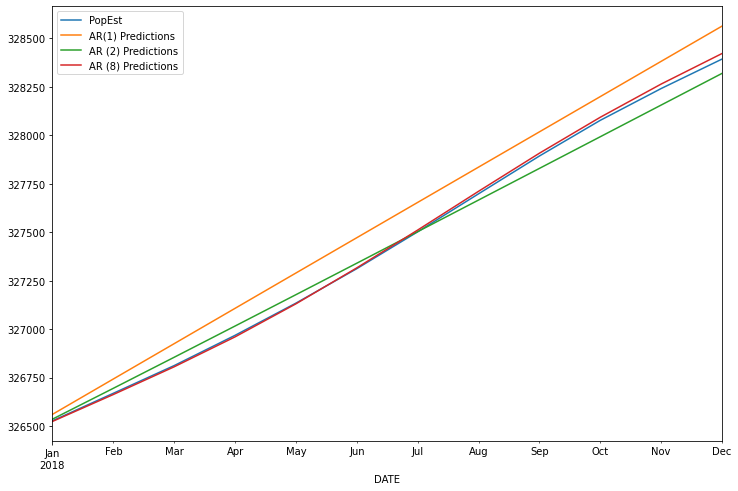

<AxesSubplot:xlabel='DATE'>

const 82.309677

L1.PopEst 2.437997

L2.PopEst -2.302100

L3.PopEst 1.565427

L4.PopEst -1.431211

L5.PopEst 1.125022

L6.PopEst -0.919494

L7.PopEst 0.963694

L8.PopEst -0.439511

dtype: float64

AR1 MSE was : 17449.714239577344

AR2 MSE was : 2713.258615675103

AR8 MSE was : 186.97377437908688

<AxesSubplot:xlabel='DATE'>

<AxesSubplot:xlabel='DATE'>

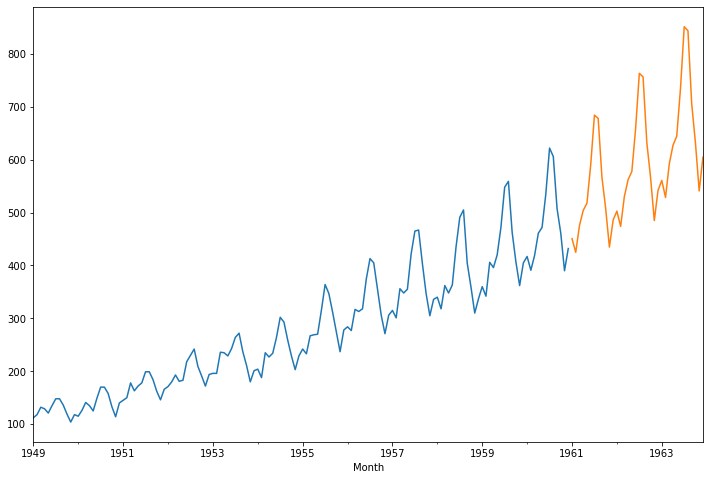

<AxesSubplot:xlabel='Month'>

(0.8153688792060512,

0.991880243437641,

13,

130,

{'1%': -3.4816817173418295,

'5%': -2.8840418343195267,

'10%': -2.578770059171598},

996.692930839019)

Help on function adfuller in module statsmodels.tsa.stattools:

adfuller(x, maxlag=None, regression='c', autolag='AIC', store=False, regresults=False)

Augmented Dickey-Fuller unit root test.

The Augmented Dickey-Fuller test can be used to test for a unit root in a

univariate process in the presence of serial correlation.

Parameters

----------

x : array_like, 1d

The data series to test.

maxlag : int

Maximum lag which is included in test, default 12*(nobs/100)^{1/4}.

regression : {"c","ct","ctt","nc"}

Constant and trend order to include in regression.

* "c" : constant only (default).

* "ct" : constant and trend.

* "ctt" : constant, and linear and quadratic trend.

* "nc" : no constant, no trend.

autolag : {"AIC", "BIC", "t-stat", None}

Method to use when automatically determining the lag.

* if None, then maxlag lags are used.

* if "AIC" (default) or "BIC", then the number of lags is chosen

to minimize the corresponding information criterion.

* "t-stat" based choice of maxlag. Starts with maxlag and drops a

lag until the t-statistic on the last lag length is significant

using a 5%-sized test.

store : bool

If True, then a result instance is returned additionally to

the adf statistic. Default is False.

regresults : bool, optional

If True, the full regression results are returned. Default is False.

Returns

-------

adf : float

The test statistic.

pvalue : float

MacKinnon"s approximate p-value based on MacKinnon (1994, 2010).

usedlag : int

The number of lags used.

nobs : int

The number of observations used for the ADF regression and calculation

of the critical values.

critical values : dict

Critical values for the test statistic at the 1 %, 5 %, and 10 %

levels. Based on MacKinnon (2010).

icbest : float

The maximized information criterion if autolag is not None.

resstore : ResultStore, optional

A dummy class with results attached as attributes.

Notes

-----

The null hypothesis of the Augmented Dickey-Fuller is that there is a unit

root, with the alternative that there is no unit root. If the pvalue is

above a critical size, then we cannot reject that there is a unit root.

The p-values are obtained through regression surface approximation from

MacKinnon 1994, but using the updated 2010 tables. If the p-value is close

to significant, then the critical values should be used to judge whether

to reject the null.

The autolag option and maxlag for it are described in Greene.

References

----------

.. [1] W. Green. "Econometric Analysis," 5th ed., Pearson, 2003.

.. [2] Hamilton, J.D. "Time Series Analysis". Princeton, 1994.

.. [3] MacKinnon, J.G. 1994. "Approximate asymptotic distribution functions for

unit-root and cointegration tests. `Journal of Business and Economic

Statistics` 12, 167-76.

.. [4] MacKinnon, J.G. 2010. "Critical Values for Cointegration Tests." Queen"s

University, Dept of Economics, Working Papers. Available at

http://ideas.repec.org/p/qed/wpaper/1227.html

Examples

--------

See example notebook

ADF Test Statistic 0.815369

p-value 0.991880

# Lags Used 13.000000

# Observations 130.000000

critical value (1%) -3.481682

critical value (5%) -2.884042

critical value (10%) -2.578770

dtype: float64

from statsmodels.tsa.stattools import adfuller

def adf_test(series, title=''):

"""

Pass in a time series and an optional title, returns an ADF report

"""

print(f'Augmented Dickey-Fuller Test: {title}')

result = adfuller(series.dropna(), autolag = 'AIC')

labels = ['ADF test statistic', 'p-value', '# lags used', '# obervations']

out = pd.Series(result[0:4], index = labels)

for key, val in result[4].items():

out[f'critical value ({key})'] = val

print(out.to_string())

if result[1] <= 0.05:

print('Strong evidence against the null hypothesis')

print('Reject the null hypothesis')

print('Data has no unit root and is stationary')

else:

print('Weak evidence against the null hypothesis')

print('Fail to reject the null hypothesis')

print('Data has a unit root and is non-stationary')

Augmented Dickey-Fuller Test:

ADF test statistic 0.815369

p-value 0.991880

# lags used 13.000000

# obervations 130.000000

critical value (1%) -3.481682

critical value (5%) -2.884042

critical value (10%) -2.578770

Weak evidence against the null hypothesis

Fail to reject the null hypothesis

Data has a unit root and is non-stationary

<AxesSubplot:xlabel='Month'>

<AxesSubplot:xlabel='Date'>

Augmented Dickey-Fuller Test:

ADF test statistic -4.808291

p-value 0.000052

# lags used 6.000000

# obervations 358.000000

critical value (1%) -3.448749

critical value (5%) -2.869647

critical value (10%) -2.571089

Strong evidence against the null hypothesis

Reject the null hypothesis

Data has no unit root and is stationary

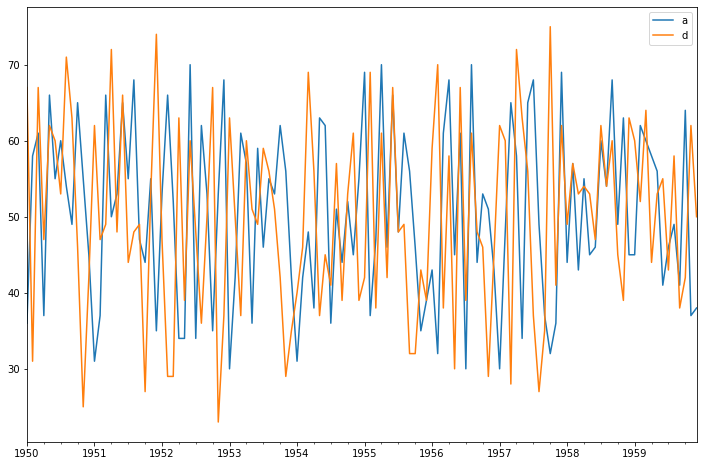

Granger Causality

number of lags (no zero) 1

ssr based F test: F=1.7051 , p=0.1942 , df_denom=116, df_num=1

ssr based chi2 test: chi2=1.7492 , p=0.1860 , df=1

likelihood ratio test: chi2=1.7365 , p=0.1876 , df=1

parameter F test: F=1.7051 , p=0.1942 , df_denom=116, df_num=1

Granger Causality

number of lags (no zero) 2

ssr based F test: F=286.0339, p=0.0000 , df_denom=113, df_num=2

ssr based chi2 test: chi2=597.3806, p=0.0000 , df=2

likelihood ratio test: chi2=212.6514, p=0.0000 , df=2

parameter F test: F=286.0339, p=0.0000 , df_denom=113, df_num=2

Granger Causality

number of lags (no zero) 3

ssr based F test: F=188.7446, p=0.0000 , df_denom=110, df_num=3

ssr based chi2 test: chi2=602.2669, p=0.0000 , df=3

likelihood ratio test: chi2=212.4789, p=0.0000 , df=3

parameter F test: F=188.7446, p=0.0000 , df_denom=110, df_num=3

Granger Causality

number of lags (no zero) 1

ssr based F test: F=1.5225 , p=0.2197 , df_denom=116, df_num=1

ssr based chi2 test: chi2=1.5619 , p=0.2114 , df=1

likelihood ratio test: chi2=1.5517 , p=0.2129 , df=1

parameter F test: F=1.5225 , p=0.2197 , df_denom=116, df_num=1

Granger Causality

number of lags (no zero) 2

ssr based F test: F=0.4350 , p=0.6483 , df_denom=113, df_num=2

ssr based chi2 test: chi2=0.9086 , p=0.6349 , df=2

likelihood ratio test: chi2=0.9051 , p=0.6360 , df=2

parameter F test: F=0.4350 , p=0.6483 , df_denom=113, df_num=2

Granger Causality

number of lags (no zero) 3

ssr based F test: F=0.5333 , p=0.6604 , df_denom=110, df_num=3

ssr based chi2 test: chi2=1.7018 , p=0.6365 , df=3

likelihood ratio test: chi2=1.6895 , p=0.6393 , df=3

parameter F test: F=0.5333 , p=0.6604 , df_denom=110, df_num=3

17.02

4.125530268947253

3.54

<AxesSubplot:xlabel='Month'>